The First-Time Buyer Isn’t Gone. The Timeline Has Shifted

For much of the past four decades, the American housing market relied on a steady assumption: first-time buyers would account for roughly 40% of activity. They were the entry point—the mechanism through which demand refreshed itself and the ownership cycle advanced.

That assumption no longer holds.

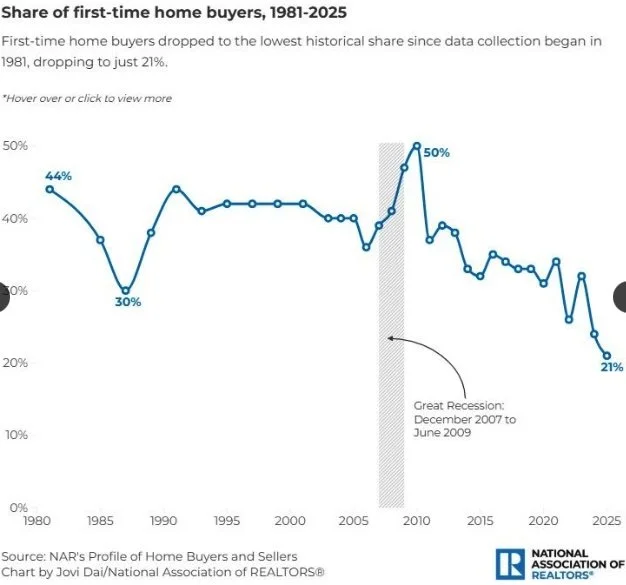

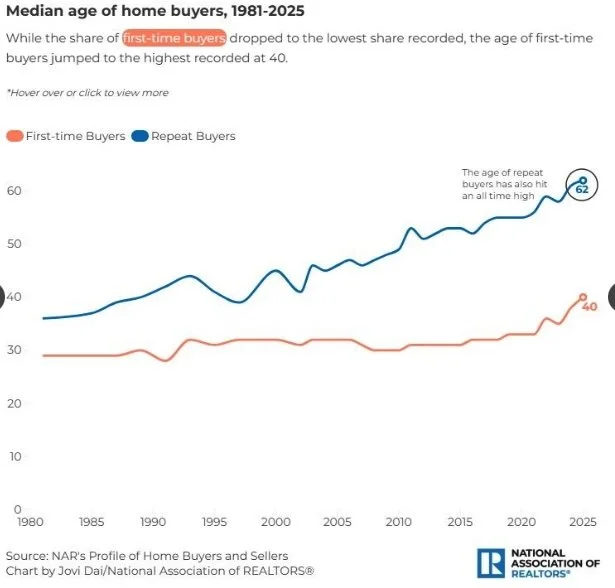

Recent data from National Association of Realtors indicates that first-time buyers now represent just 21% of the market. At the same time, the median age of a first-time purchaser has risen to 40. The significance of these figures is not simply that housing has become more expensive, or that borrowing costs have increased. Those conditions, while important, are not new in isolation. What is new is the cumulative effect.

The entry into homeownership has been deferred.

A Market Defined by DelaY

The decline in first-time participation suggests a structural shift rather than a cyclical one. In prior periods of rising rates or limited supply, first-time buyers often receded temporarily, only to return as conditions stabilized.

What is occurring now appears different.

Prospective buyers are not exiting the market altogether—they are postponing entry, often by a decade or more. The typical first-time buyer is no longer in their late twenties or early thirties, but well into midlife.

This delay alters the rhythm of the housing market itself.

Renters remain renters longer

Equity accumulation begins later

Move-up transactions are pushed further into the future

The result is a slower turnover of housing stock and a compression of demand into higher price tiers.

Constraints at the Entry Point

Three forces appear to be converging: Affordability has deteriorated as home prices and interest rates have risen in tandem, increasing the cost of entry in absolute and monthly terms. Inventory, particularly at the lower end of the market, remains constrained. Existing homeowners, many of whom are locked into historically low mortgage rates, have little incentive to sell. Time horizons have lengthened. Saving for a down payment now takes longer, and buyers are more cautious in committing to ownership under uncertain conditions. Individually, these factors are manageable. Together, they redefine access.

Implications Beyond Housing

The implications extend beyond the housing market. Homeownership has historically functioned as a primary vehicle for household wealth accumulation in the United States. Delayed entry into ownership delays that process. Over time, this may widen disparities between those who enter the market earlier and those who do not. It also reshapes expectations. A generation that once anticipated buying in its late twenties may now view ownership as a mid-career milestone.

A Market That Requires Strategy

It would be easy to interpret these conditions as prohibitive. That conclusion, however, overlooks a key point. Markets do not eliminate entry points—they reposition them. What has changed is not the existence of opportunity, but the path to it. Buyers who succeed in this environment are less reliant on timing and more dependent on planning: how they structure financing, where they choose to enter, and how they compete. In that sense, the market is not closed. It is more selective.

Conclusion

The first-time buyer has not disappeared. But the timeline has shifted, and with it, the dynamics of the broader market. Whether this proves to be a lasting realignment or a prolonged phase will depend on the interaction of rates, supply, and income growth in the years ahead. For now, the data suggests a simple, if consequential, reality:

Homeownership remains attainable—but it arrives later, and it demands more intention than it once did.

Source: